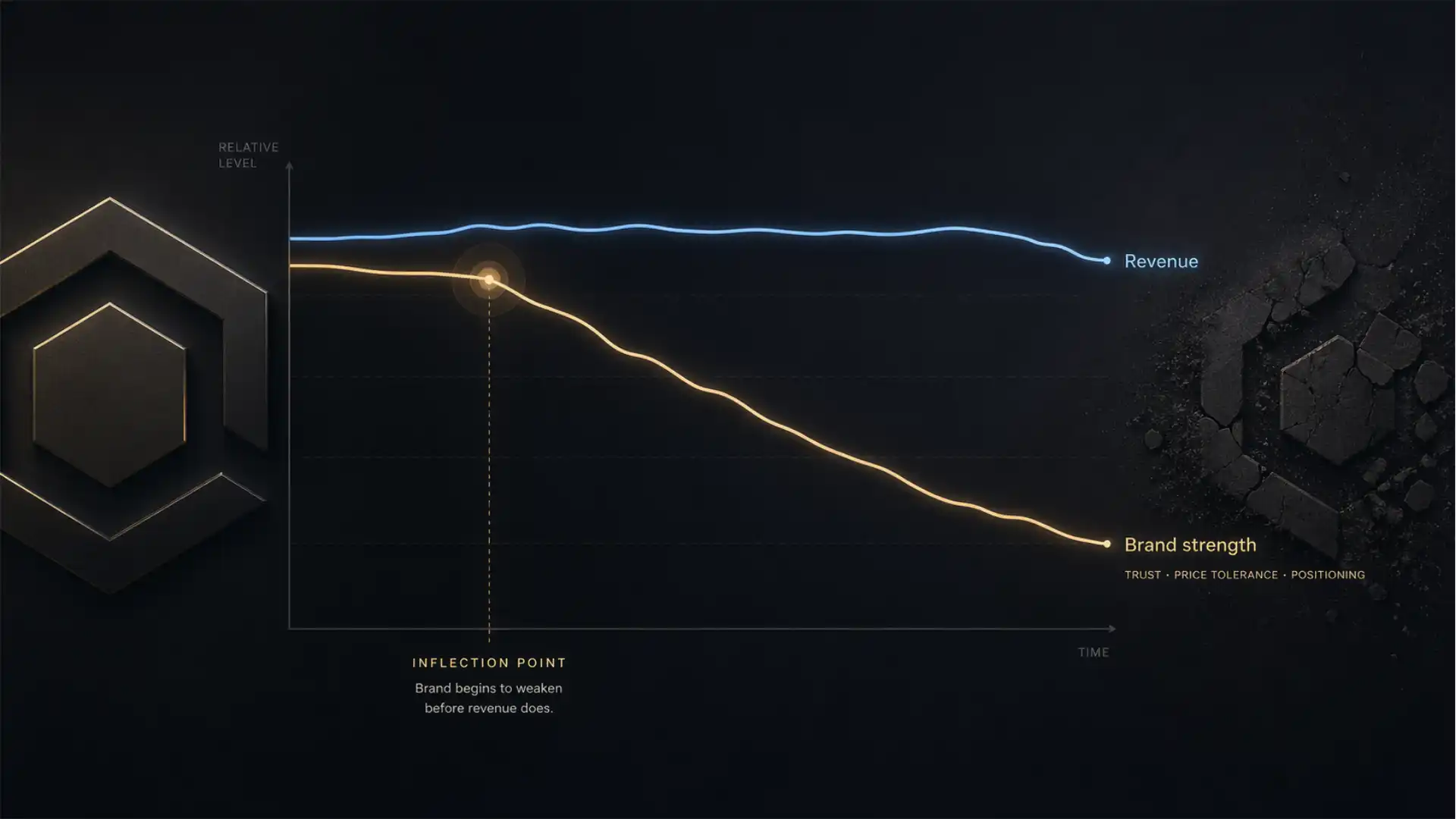

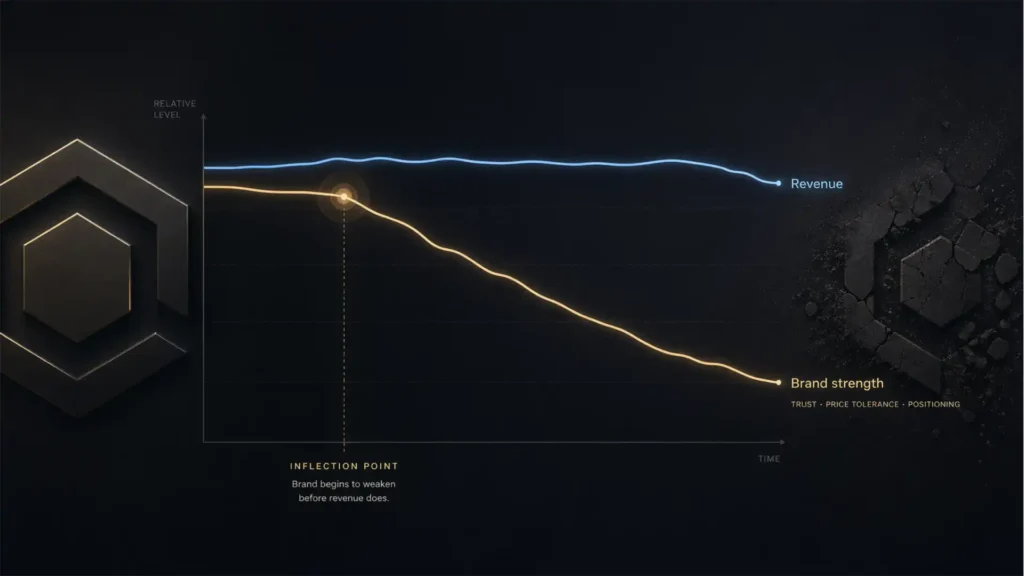

Most positioning failures do not show up first in revenue. Revenue can stay alive on repeat customers, channel expansion, discounts, enterprise contracts, heavy promotions, or a sharp performance team that keeps harvesting existing demand. That lag is exactly what makes brand decay expensive. By the time finance sees weakness, the brand has often already lost ground in memory, price acceptance, search demand, and customer confidence. Research from Nielsen, Thinkbox, Google, and BCG all points toward the same pattern: the market usually notices a weakening brand before the income statement does.

Table of Contents

A strong position is not the line in the brand deck. It is the set of shortcuts buyers retrieve when they need to choose. Once those shortcuts get blurry, three things start happening fast: customers need more persuasion, more discounting, and more reminders; acquisition gets harder; and the promise made in marketing stops matching the experience delivered in product, sales, service, or retail. Revenue can still look respectable during that period, which is why weak positioning often gets misdiagnosed as a pricing issue, a media issue, or a sales execution issue.

Revenue flatters a weakening brand

Revenue is a lagging outcome with many temporary supports beneath it. Existing customers keep buying out of habit. Sales teams work accounts harder. Promotions pull demand forward. Distribution gains can offset lower preference. A marketplace listing or a retail expansion can keep units moving even while the brand itself is becoming less meaningful. None of that proves the position is healthy. It only proves the business still has ways to convert demand that was built earlier or demand created elsewhere in the system.

That delay is not a theory problem. It is a measurement problem and a management problem. Binet and Field’s work on short- and long-term effects warned years ago that brands get misled when they steer by short-term response measures alone. Nielsen has repeated the same warning in current marketing research: pull back on brand building, and awareness and consideration soften first, while future sales weaken later. Google’s work with marketers using long-term models makes the point even more plainly: the health metrics that move first are things like unaided awareness, consideration, familiarity, and share of search. Revenue usually follows behind.

That is why teams get false comfort from a decent quarter. A decent quarter can be financed by past brand strength. It can also be financed by discounting away margin, exhausting paid demand, or leaning on channels that do not care much about preference. The danger sits in the gap between commercial output and brand condition. When that gap widens, leadership starts reading resilience where the market is actually signaling decay. A strong quarter can be the residue of yesterday’s positioning, not proof of today’s.

Positioning lives in memory, not in slide decks

Positioning is often discussed as messaging, but buyers do not shop inside a positioning framework. They shop with memory, habit, cues, and category triggers. Kevin Keller’s classic work on customer-based brand equity defined brand strength in terms of brand knowledge and the differential response it produces in the market. Ehrenberg-Bass research pushes the same conversation into buying behavior: brands grow when they are easy to think of and easy to buy, which is why mental and physical availability matter so much. BCG’s work on mind share reaches a similar conclusion from a different angle: the first brand that comes to mind in a relevant demand space has a strong advantage in choice.

That matters because brand decline rarely begins with an obvious public collapse. It starts when the brand’s memory structures become narrower, weaker, or less useful. Buyers stop retrieving the brand in as many situations. They still recognize it, but they no longer feel pulled toward it. They remember the logo without feeling the reason. They recall the name after seeing the shelf, but not before. They choose it when discounted, not when full-priced. They describe it in generic language that could fit three competitors just as well. That is positioning damage. It has already begun even if sales reports still look calm.

A lot of internal confusion starts right there. Companies think they need a sharper slogan, a new campaign, or a more emotional message. Sometimes they do. Yet the real issue is often simpler: the brand has stopped owning enough useful associations in the buyer’s mind. That can come from overextension, inconsistent execution, product drift, pricing changes the brand has not earned, or years of media that entertained without clearly branding the message. None of those problems will be fixed by a prettier articulation of strategy. The market responds to retrievability, recognizability, and credibility, not to the elegance of internal language.

The first crack usually shows up in pricing tolerance

Price is where a weak position gets exposed with brutal honesty. When buyers no longer feel the brand is worth the ask, the business starts paying a tax. That tax shows up as heavier promotion, slower conversion, more friction in sales conversations, lower renewal confidence, and a constant need to justify what used to feel natural. Kantar puts the issue plainly: a brand’s greatest strength is how well it justifies its price point. Their pricing power work also shows that many brands drift into vulnerable territory when brand equity no longer supports their actual price.

That is not only a consumer packaged goods problem. Bain’s “Elements of Value” reminds us that customers weigh perceived value against asking price, and Deloitte’s work shows that a large share of perceived value comes from factors other than price alone, including quality, service, convenience, and trust. McKinsey’s pricing research makes the financial stakes hard to ignore: pricing is one of the strongest profit levers a company has, and effective pricing work can materially lift return on sales. A brand with real position can sustain price with less panic. A brand with shaky position ends up negotiating with the market every day.

This is why some businesses misread a margin problem as a pricing problem when it is really a positioning problem. They ask, “Can we charge more?” when the sharper question is, “Have we earned the right to charge this much in the buyer’s mind?” If the answer is slipping, a clever pricing architecture may buy time, but it will not restore the missing justification. Pricing can express brand strength. It cannot manufacture it for long. Once the market senses misalignment between promise and price, the brand gets dragged toward the middle, where comparison becomes more mechanical and more brutal.

Promotions can keep the line moving while the brand gets weaker

Promotions are useful. They can drive trial, clear inventory, create urgency, and defend shelf space. The problem starts when leadership begins using them as proof that the brand is fine. Promotions can mask softening preference for longer than many teams expect. Units move. Revenue holds. The campaign dashboard looks alive. Yet each extra discount teaches the market a lesson about the true willingness to pay. Over time the customer starts asking a dangerous question: why buy this brand without a deal?

Research on promotion effectiveness complicates the usual story in an important way. Stronger brands often get more lasting benefit from promotional activity than weaker brands do, because brand equity changes how promotions are interpreted and remembered. Slotegraaf and Pauwels found that both permanent and cumulative sales effects from promotions are greater for brands with higher equity. That sounds like good news for brand owners, but it carries a warning. If a brand with weakening equity leans harder on promotion, it may get the volume lift without the durable brand benefit, while still teaching the customer to wait for a deal.

That is the trap. Promotion is not the enemy; promotion in place of position is. A healthy brand uses pricing and promotions selectively, from a place of strength. A weakening brand uses them as life support. You can spot the difference in the internal tone. Strong brands ask whether a deal supports the broader commercial strategy. Weak brands ask how much discount is needed to hit the month. Once that shift happens, the brand is no longer shaping demand. It is renting it.

Search behavior notices the drift before the finance team does

Search data is not a perfect window into brand strength, but it is one of the fastest and cheapest directional signals available. Les Binet’s work on share of search gave marketers a useful frame: movements in organic search interest often precede movements in market share, sometimes by months and in some categories by as much as a year. Google’s own work on long data and share of search backs that relationship. The value is not mystical. Search sits closer to real buyer behavior than many survey measures do. People search when curiosity, need, uncertainty, or intent rises.

That makes search valuable as an early-warning system. If branded search weakens while spend rises, something is off. If the brand keeps gaining clicks only through heavier paid support, something is off. If generic category search grows while the brand’s organic share slips, the problem may not be awareness alone. The market may be looking for solutions without instinctively reaching for your name. Subway’s work with long-term modeling is useful here because it connects media effects to brand health metrics rather than only near-term sales. The companies that catch decline early usually do not wait for revenue to tell them. They watch search interest, direct traffic, brand recall, consideration, and relative conversion efficiency as a set.

Search is also good at exposing narrative drift. When buyers start pairing your brand name with “reviews,” “problems,” “complaints,” “alternative,” or “vs,” the market is doing diagnostic work on you. That often shows up before churn spikes. Brand teams sometimes ignore that because the total query volume still looks healthy. They should not. Demand is not the same as confidence. A brand can still be searched while losing authority. Search tells you whether you remain the natural answer or have become a question mark.

Distinctive assets fade quietly

Brands do not only lose through meaning. They also lose through recognition failure. Distinctive assets — colors, shapes, sounds, characters, taglines, packaging structures, recurring visual codes — act like retrieval shortcuts. Ehrenberg-Bass research has been consistent on this point: advertising must be associated with the brand behind it, and many brands still underperform on recognition. Their work on distinctive assets shows that only a small number of brand cues are strong enough to substitute for the brand name. Most brands need more repetition, more co-presentation, and more consistency than they currently allow themselves.

This is where internal tastes often sabotage external memory. A team gets bored with an asset long before the market has properly learned it. So the code changes. Packaging gets “refreshed.” The brand voice gets loosened. The logo is minimized in the name of elegance. Campaigns become creatively varied but structurally unlinked. Each move can look defensible in isolation. Together they erode recognizability. McKinsey’s design work matters here because design is not decoration in this context; it is commercial infrastructure. Companies that treat design as a serious business capability tend to outperform because design shapes recognition, ease, consistency, and trust across the whole experience.

Once distinctive assets weaken, everything gets more expensive. Media has to work harder. Packaging has to shout louder. Sales conversations need more explanation. Search has to pick up more of the load. That is a hidden cost of bad brand management that rarely shows up in the creative review. When the brand is not quickly recognizable, every channel is forced to compensate. Leaders often treat this as a media efficiency problem. Very often it is a brand memory problem.

Category entry points start collapsing

A brand does not need to own every possible buying moment in a category, but it does need enough relevant entry points to stay mentally available. Ehrenberg-Bass puts this in concrete terms: category entry points are the buying situations, motives, needs, or occasions that bring a category to mind. A brand becomes easier to buy when it connects itself to more of those moments. Buyers do not wake up asking for “the most strategically positioned brand.” They ask for something for dinner, for a quick fix, for a safe choice, for a premium gift, for help with a problem, for something that feels like them. If your brand is not retrieved in enough of those moments, the position is already narrowing.

This narrowing happens more often than companies think. Many brands begin with a vivid association, grow on that basis, then stop building beyond it. Over time the association that once felt sharp becomes confining. The brand is remembered for one use case, one audience, one price tier, or one old story about itself. Sales may continue because legacy buyers still know the path. New demand gets harder to win because the brand is no longer top of mind in the wider set of buying contexts that now matter. That is a positioning problem even when brand tracking still shows decent awareness. Awareness without useful retrieval is flimsy.

This is also why “differentiation” gets overstated in boardrooms. Buyers do not always reward a brand for being intellectually distinct. Often they reward the brand that is simply easier to remember and easier to find in the right buying moment. A lot of bad repositioning work comes from trying to sound more unique rather than becoming more available in memory. Sharp positioning is not always about saying something no rival says. Sometimes it is about being the brand that arrives fastest and feels most natural in the purchase situation.

The customer journey begins telling a different story

Brands promise with words, but they collect trust through experience. That is why positioning can break even while communications remain polished. The ad still says the right thing. The homepage still looks on-brand. The problem sits in the lived path. McKinsey’s work on customer journeys found that performance on journeys is substantially more predictive of customer satisfaction and churn than performance on individual touchpoints. That is a brutal finding for companies that measure channels separately, because customers do not live in functional silos. They experience the whole arc.

Once the journey drifts from the promise, positioning starts losing credibility. A premium brand with clumsy service. A simple product with a messy onboarding flow. A trusted brand with evasive billing language. A thoughtful brand with indifferent frontline staff. Any one of these gaps can be dismissed as execution noise. Repeated enough, the market starts updating its understanding of the brand. McKinsey’s experience-led growth work argues that improving existing customer experience is a major growth lever in commoditizing markets, which is another way of saying that the lived experience often becomes the brand’s most persuasive positioning proof.

BCG’s work on touchpoints points in the same direction. When brands fail to translate their intended position across the full path to purchase, they create disjointed execution and weaker returns. That failure does not always show up as an immediate sales crash. It first appears as friction, lower recommendation confidence, softer loyalty, and a need for the next campaign to explain what the brand already claimed last quarter. Customers do not need a new message at that stage. They need a brand that behaves like itself everywhere they meet it.

Internal language gets fuzzy before the market goes cold

A weakening position is often audible inside the company before it becomes obvious outside it. Ask product, sales, customer support, performance marketing, retail partners, and leadership to describe the brand in one sentence. Healthy brands produce different phrasing but recognizable alignment. Weakening brands produce competing answers. One team talks about price. Another talks about innovation. Another talks about trust. Another says convenience. The support team describes what people actually praise, and that answer barely overlaps with the campaign. When the organization stops describing the same promise, the market usually follows.

That internal fuzziness creates two kinds of waste. First, money gets spread across too many claims. Second, customer experience becomes uneven because each team is trying to express a different version of value. BCG’s work on purpose, trust, and stakeholder perceptions is useful here because it frames value as something built through repeated alignment between what the company says, what stakeholders expect, and what the company visibly does. Trust research from BCG also shows that stakeholder perception is dynamic and shaped by signals far beyond formal communications. So a brand can still sound consistent in its owned language while being interpreted very differently in the market.

The fix is rarely “better messaging” alone. It usually requires stripping back to fewer, more defensible associations and then making sure product, experience, pricing, and communications all cash the same check. Internal clarity matters because positioning is not a campaign function. It is a coordination function. When internal language gets muddy, the brand begins paying interest on that confusion across every customer-facing channel.

Performance marketing makes the damage easy to miss

Performance marketing is useful, measurable, and often commercially necessary. It also makes brand erosion easier to hide because it is excellent at harvesting existing intent. If the category still has demand and the business still has brand residue, lower-funnel tactics can keep revenue respectable while upper-funnel brand health weakens. That does not make performance marketing the problem. The problem appears when leaders start using harvest signals as proof that the field is still fertile.

Nielsen’s recent work shows that marketers continue to feel the pressure between immediate revenue and brand awareness, with regional differences in how heavily they lean toward short-term outcomes. Their broader argument is steady across reports: brand building and performance are interdependent. When marketers overfavor measurable lower-funnel tactics, they can underinvest in the channels and activities that keep the brand strong enough for performance to work efficiently later. Binet and Field reached the same broad conclusion years earlier from a different evidence base. Short-term metrics can steer companies toward actions that look efficient now while quietly hurting long-term profitability and market share growth.

That is why weak brands often report “acceptable acquisition” until suddenly they do not. The cost curve does not rise in a perfectly smooth line. It gets masked by targeting, retargeting, promo bursts, channel shifts, and creative changes. Then the floor drops because the underlying demand pool is thinner and less brand-biased than leadership thought. When that happens, companies often react by pushing harder on performance, which deepens the trap. You cannot keep harvesting a field you stopped planting.

Satisfaction and trust are commercial signals, not soft ones

Some executive teams still treat satisfaction and trust like qualitative side notes while they reserve real attention for sales, margin, and retention. That split makes no sense anymore. The American Customer Satisfaction Index is built on the premise that customer satisfaction is predictive, not ornamental, and its own site describes ACSI as a proven predictor of financial performance. The academic literature around ACSI goes further. Fornell, Morgeson, and Hult found long-run outperformance associated with higher customer satisfaction, and other work has connected satisfaction to cash flow, shareholder value, and the way markets price firms.

Trust sits in the same commercial category. Edelman’s research found trust ranked alongside cost and quality as a purchase consideration in its global 2025 brand trust work, while earlier Edelman reporting described trust as second only to price for evaluating a new brand. BCG’s trust research adds a harder operating lens: trust is dynamic, difficult to rebuild, and increasingly measurable through ongoing stakeholder signals. A business that loses trust often does not lose all revenue at once. It loses something more dangerous first — the benefit of the doubt. After that, every mistake carries more weight and every promise needs more proof.

Positioning sits right on top of these dynamics. If the brand claims confidence, reliability, premium quality, fairness, or simplicity, satisfaction and trust tell you whether the market believes it. They are not just downstream sentiment measures. They are live audits of whether the position still holds under real experience. A brand that slips here may keep selling for a while, especially if switching costs are high. Yet the strategic damage is already running.

The middle of the market punishes vagueness

Brands can sometimes survive with blunt positioning at the edges. A very cheap offer can win on price. A very prestigious offer can win on status, craft, or exclusivity. The middle is harsher. In the middle, buyers compare more and forgive less. If the brand has weak distinctiveness, weak pricing power, and a vague reason to matter, it gets squeezed from both sides. Kantar’s work on differentiation and pricing power is useful here because it shows the commercial value of being meaningfully different in ways the market will reward, especially when that difference supports willingness to pay.

This does not contradict the Ehrenberg-Bass focus on distinctiveness and availability. The two ideas meet in the real market. A brand needs to be easy to notice, easy to remember, and credible enough to justify its place. Bain’s value hierarchy adds another angle: customers weigh many dimensions of value, not just function and price. When a middle-market brand stops being clear on which value it disproportionately delivers, comparison becomes more transactional. Buyers then default to distribution convenience, reviews, promotions, or whichever rival has cleaner cues.

That is why many respectable businesses end up sounding broader as they get weaker. They try to appeal to everybody because nobody is pulling hard enough. The result is language that offends no one and moves no one. The offer becomes competent but forgettable. Revenue may hold because the business still has shelf space, traffic, or an installed base. The position is already thinning out. In crowded categories, vague brands are expensive brands to run.

Growth channels can hide strategic decay

A brand can look commercially healthy because distribution is doing the work. Rajavi and colleagues found in their work on brand equity across good and bad times that distribution breadth is one of the strongest brand factors, especially during contractions. Ehrenberg-Bass has long argued that physical availability matters alongside mental availability. Put those together and you get a useful warning: more points of sale, more SKUs, more channel partners, or more territories can keep the business moving even when the brand’s position is getting weaker in the buyer’s mind.

This matters a lot in founder-led businesses and scale-stage companies. Expansion can hide drift. New resellers join. New paid channels open. New markets are entered. Marketplace volume arrives. The top line grows, but the core brand gets less coherent with each step. Soon the company mistakes channel performance for brand health. Then a new competitor enters, a retailer changes terms, paid acquisition gets pricier, or macro conditions tighten, and the hidden weakness is exposed. The company has scale without enough preference. That is a fragile place to be.

The same thing happens with product sprawl. More assortment can support revenue, yet every added variation asks the brand to stay coherent across more use cases and more customer expectations. When the additions are not tied back to a clear promise, the brand becomes easier to stock than to understand. That is not growth. It is complexity wearing a growth costume.

Measurement needs leading indicators, not only outcomes

A company serious about brand position cannot wait for lagging outcomes alone. Revenue, conversion, CAC, retention, and margin all matter, but they tell you what the business achieved after the market already processed your brand. By then, the correction is slower and more expensive. Better systems pull forward the measurement. BCG’s FFR work is notable because it is built around detecting shifts in buying associations within weeks, not quarters. Google’s work with marketers using long-term models points toward the same need to track awareness, consideration, and familiarity alongside sales. ACSI exists for the same reason in customer experience. Leading indicators matter because brands erode upstream.

The most useful leading indicators are not mysterious. They are usually a mix of mental availability, price acceptance, search behavior, customer confidence, and execution consistency. Share of search gives you one behavioral lens. Relative willingness to pay gives you another. Distinctive asset recognition matters because you cannot be chosen easily if you are not recognized quickly. Journey satisfaction matters because the market adjusts brand meaning based on lived friction. None of these alone tells the whole story. Together they can show the direction of travel well before revenue announces it.

The key is to stop asking each metric to act like a verdict. Brand health is rarely visible in a single number. It is visible in a pattern. If branded search is softening, discounting is rising, willingness to pay is slipping, review language is getting more generic, and customer service is carrying the promise that marketing used to carry, the brand is telling you something. A business that only watches outcomes will always find out late.

The signals worth watching every month

Leaders do not need fifty brand metrics. They need a tight set that tells the truth early. The most useful signals are the ones that move before volume falls off a cliff and before margin has been permanently trained downward.

Early signals that move before revenue

| Early signal | What usually changed first | What the business often misreads it as | What shows up later |

|---|---|---|---|

| Branded search softens | The brand is less top-of-mind in relevant buying moments | A temporary media issue | Lower market share and weaker organic demand |

| More discounting needed to convert | Price is no longer fully justified by brand strength | A pure pricing problem | Margin pressure and lower perceived value |

| Distinctive assets test weakly | Recognition and recall are eroding | A creative refresh issue | Higher media waste and slower conversion |

| Fewer category entry points feel natural | The brand is only remembered in a narrow set of occasions | A messaging problem | Smaller consideration set and slower growth |

| Journey satisfaction slips | Experience no longer matches the brand promise | A service or ops issue only | Churn, weaker trust, lower advocacy |

| Internal descriptions of the brand diverge | The organization no longer shares one commercial promise | A communication alignment issue | Inconsistent execution across channels |

That table matters because it separates movement in the brand from movement in the spreadsheet. The second tends to trail the first. Companies that treat those early shifts as operational noise usually end up paying for the delay with higher acquisition costs, heavier promotion, and a more expensive repositioning effort later on.

Repair starts with subtraction

When leaders realize the position is slipping, the first instinct is often additive. Add more messages. Add more campaigns. Add more proof points. Add more segments. Add more product variants so more people see themselves in the brand. That usually makes the problem worse. Weak positions do not recover because the brand said more things to more audiences. They recover because the brand became easier to understand, easier to remember, and easier to trust again.

Repair usually starts with subtraction. Fewer claims. Fewer audience fantasies. Fewer design deviations. Fewer reasons for the market to wonder what business you are actually in. Kantar’s work on difference is useful here because difference has to be linked to commercial payoff, not to internal novelty. Ehrenberg-Bass work on distinctive assets carries the same discipline in execution: commit to the codes that help people recognize you and stop changing them because the team got restless. BCG’s demand-space thinking adds another layer: know the specific contexts in which you most need to be the first brand retrieved, and build from there rather than speaking in broad, flattering abstractions.

None of this is glamorous. It is usually slower and less theatrical than a “brand refresh.” Yet it is much closer to what the market actually rewards. A repaired position feels simpler on the outside and more demanding on the inside, because it requires the company to align product, pricing, experience, media, and sales around a narrower truth. The brand gets stronger when the business becomes more disciplined, not when the language becomes more elaborate.

Recovery costs more than most leaders expect

Brand decline is cheap to ignore for a while and expensive to reverse. BCG warns that delayed, backward-looking brand measurement puts investment at risk and notes that recovering lost brand momentum can cost materially more than what was saved. Nielsen’s long-term brand-building research says recovery from extended periods of not advertising can take years. BCG’s trust research is equally blunt on the emotional side of the ledger: once trust drops sharply, rebuilding is slow and difficult. None of this should surprise anyone who has tried to win back a buyer who no longer gives the brand easy credit.

That is why “we can fix it later” is one of the most expensive sentences in brand management. Later usually means the market has already updated its beliefs. Buyers have already learned to wait for a discount, switch to a rival, or describe you in generic terms. Retailers have already started treating you as replaceable. Staff have already stopped speaking about the brand with one voice. By then the business is not just rebuilding awareness. It is rebuilding belief, recognition, price legitimacy, and internal discipline all at once.

The companies that avoid this bill are not always the loudest brands or the most creative ones. They are usually the ones that respect the lag. They understand that revenue can flatter them. They use early signals to course-correct while the business still has room. They do not wait for the quarter to become a crisis before they admit the position has already shifted.

A strong brand is easier to buy, not easier to describe

The cleanest way to think about positioning is not as rhetoric but as buying ease. A strong brand is easier to think of in the right moment, easier to recognize quickly, easier to justify at the asked price, easier to trust through the journey, and easier for every team inside the company to express in consistent ways. Keller’s brand equity work, Ehrenberg-Bass research on mental and physical availability, Google’s evidence on share of search, Kantar’s work on pricing power, and McKinsey’s journey research all converge on that point from different directions. Brand strength lowers the cognitive and commercial effort required to choose you.

That is also why revenue is such a poor first alarm. Revenue can keep showing momentum while buying ease is quietly declining. Buyers can still find you while feeling less sure. They can still purchase while resenting the price. They can still convert while needing more reminders, more discounting, and more paid prompts than they used to. A spreadsheet can tolerate that for a while. The brand cannot. Eventually the gap closes, and when it does, leaders act shocked by a decline that started much earlier in memory and meaning.

The smart move is not paranoia. It is respect for sequence. First the position weakens in the mind. Then it weakens at the price point. Then it weakens in search, in satisfaction, in trust, in conversion efficiency, in channel power, and finally in revenue. By the time revenue confirms the problem, the brand has been asking for help for a long time.

Questions leaders should ask before positioning weakens

It means the first damage usually shows up in memory, price acceptance, search demand, trust, and consistency, while revenue is still being supported by repeat customers, promotions, distribution, or performance spend. The commercial decline often comes later.

Because revenue has buffers. Existing customers still buy, sales teams keep accounts alive, discounts pull demand forward, and channel expansion can add volume. Those forces can hide a weaker market position for months or quarters.

Price tolerance is often one of the clearest early signs. When customers need more discounting or more explanation to accept the same price, brand strength is usually softening. Search behavior and category retrieval are also fast warning signals.

No. A brand can be known and still be weak. What matters is whether buyers retrieve it in relevant buying moments, recognize it quickly, and feel it is worth choosing at the expected price.

Share of search tracks a brand’s share of organic search interest in its category. Research presented by Les Binet and discussed by Google shows that movements in share of search often precede movements in market share, which makes it useful as an early directional signal.

They can if they become habitual support rather than selective tools. Promotions are useful, but when a brand depends on them too heavily, customers learn to separate the brand from its full price and wait for deals.

Strong positioning helps a brand justify its price. Kantar’s work frames pricing power as a core brand asset, and broader pricing research shows that companies with clearer value justification have more room to protect margin without losing demand.

Yes. Distinctive assets help buyers recognize and retrieve the brand quickly. Ehrenberg-Bass research shows that recognition is a basic condition of advertising effectiveness, and weak assets raise the cost of every media and sales effort.

They are the occasions, needs, motives, and situations that make a buyer enter the category. Brands grow when they connect themselves to more relevant entry points, because they become easier to recall in more buying moments.

Yes. If the experience does not match the promise, the market updates its belief about the brand. McKinsey found that performance on journeys is more predictive of satisfaction and churn than performance on single touchpoints.

Because performance channels can keep harvesting demand even while brand demand gets weaker. That creates the illusion of health until acquisition costs rise and the underlying preference pool gets thinner.

Yes. ACSI positions satisfaction as predictive of financial performance, and academic work has linked customer satisfaction to stock returns, cash flow, and shareholder value. Trust research also shows it affects choice and is hard to rebuild once lost.

The middle is where comparison gets harsh. A brand that is not clearly distinctive, credible, or worth its price gets squeezed by cheaper rivals on one side and stronger premium rivals on the other.

Yes. More outlets, broader assortment, or new channels can keep revenue growing even when preference is weakening. Distribution is powerful, but it can mask a brand problem rather than solve it.

Track a small set of leading signals: branded search, consideration, willingness to pay, distinctive asset recognition, category entry point coverage, journey satisfaction, and internal message consistency.

Usually the opposite. Recovery tends to start with fewer claims and tighter discipline, not more words. The brand has to become easier to understand and more consistent across product, pricing, design, and experience.

Because the company is no longer just rebuilding awareness. It is trying to rebuild recognition, trust, price legitimacy, and internal alignment after the market has already updated its view. Research from BCG and Nielsen suggests that recovery can take years and cost much more than what was saved through short-term cuts.

It looks like a brand that comes to mind naturally in relevant situations, gets recognized quickly, feels worth the price, behaves consistently through the journey, and does not need to over-explain itself to be chosen.

Author:

Jan Bielik

CEO & Founder of Webiano Digital & Marketing Agency

This article is an original analysis supported by the sources cited below

Capturing Mind Share with Precision Branding

BCG’s work on mind share and First-Fast Response as an early signal of shifts in brand associations and future choice.

Unlocking marketing effectiveness in the digital age

Google’s discussion of long data, econometrics, and the link between share of search and future market performance.

Beyond today: Why long-term marketing drives business longevity

Nielsen’s argument for brand building as a long-term revenue driver and a warning against neglecting upper-funnel health.

The three Cs of customer satisfaction: Consistency, consistency, consistency

McKinsey’s research on journeys, satisfaction, and churn across the customer experience.

Why pricing power is a brand’s greatest asset

Kantar’s explanation of pricing power as a core expression of brand strength.

Pricing power in an inflation: What’s the solution?

Kantar’s analysis of the gap between brand equity and price, with evidence on consumer willingness to pay more for stronger brands.

How do you measure ‘How Brands Grow’?

A clear summary of mental availability, physical availability, and category entry points from the Ehrenberg-Bass tradition.

Differentiation versus distinctiveness

A concise explanation of why being easy to remember and find often matters more than abstract claims of uniqueness.

5 priorities for effective advertising

Evidence-backed guidance on recognition, memory, and why branding needs to be obvious in communications.

Maximise distinctive assets

A practical look at distinctive brand assets and the discipline required to make them commercially useful.

Experience-led growth: A new way to create value

McKinsey on growth through customer experience, especially in markets where offers are becoming commoditized.

Driving Company Value with Stakeholders’ Perceptions

BCG’s case for linking purpose, trust, reputation, and stakeholder expectations to lasting business value.

BCG Trust Index | Analyzing Trust in Global Companies

An explanation of how BCG measures trust dynamically and why stakeholder perceptions matter commercially.

The Long Road to Rebuilding Corporate Trust

BCG’s analysis of how abruptly trust can fall and how difficult it is to regain.

The American Customer Satisfaction Index

The official ACSI resource describing customer satisfaction as a cross-industry, predictive business measure.

Stock Returns on Customer Satisfaction Do Beat the Market: Gauging the Effect of a Marketing Intangible

A widely cited Journal of Marketing paper linking customer satisfaction to long-run market outperformance.

Customer Satisfaction, Cash Flow, and Shareholder Value

Research connecting customer satisfaction to financial outcomes and shareholder value creation.

The Stock Market’s Pricing of Customer Satisfaction

A marketing science commentary on how financial markets interpret customer satisfaction signals.

Subway’s marketing mix modeling strategy

A practical example of connecting long-term media effects to brand health metrics such as awareness and consideration.

The 30 Elements of Consumer Value: A Hierarchy

A useful framework for understanding how customers weigh value beyond price alone.

The hidden power of pricing

McKinsey’s pricing research on margin, growth, and the commercial force of pricing strategy.

The business value of design

McKinsey’s report linking design capability to stronger financial performance and better commercial execution.

Why focusing on the entire marketing funnel is key for long-term brand growth

Nielsen’s case for balancing short-term demand capture with upper-funnel brand health.

Binet presents fast, cheap, predictive Share of Search metric

The IPA summary of Les Binet’s work on share of search as a leading indicator of market share movement.

The long and the short of it

The Thinkbox-hosted summary of Binet and Field’s influential work on long-term brand effects versus short-term response.

Think Different: The DNA of breakthrough brand value growth

Kantar’s analysis of the relationship between brand equity factors and abnormal share price returns.

Decoding Differentiation: How to unlock the brand payoff for standing out

Kantar’s work on difference, demand power, and the commercial payoff of standing out credibly.

Nielsen releases its 2025 Annual Marketing Report looking at the power of data-driven marketing

Nielsen’s summary of current marketer priorities and the tension between brand awareness and revenue growth.

Maximizing your marketing effectiveness with data-driven decision making

Nielsen’s warning that measurement bias can lead marketers to underinvest in brand equity.

A New Era for brand Trust — and a New Framework to Build It

Edelman’s framework for brand trust and its role in purchase decisions.

2026 Retail Industry Global Outlook

Deloitte’s evidence that a large share of perceived brand value comes from factors beyond price.

Conceptualizing, Measuring, and Managing Customer-Based Brand Equity

Kevin Lane Keller’s foundational article on customer-based brand equity and brand knowledge.

The Impact of Brand Equity and Innovation on the Long-Term Effectiveness of Promotions

Research showing that promotional effects differ materially depending on brand equity strength.

Brand Equity in Good and Bad Times: What Distinguishes Winners from Losers in Consumer Packaged Goods Industries?

A Journal of Marketing article on how brand factors such as distribution shape resilience across market cycles.

| Citing this article? Brief excerpts are welcome. Please credit Webiano.digital, name the author where stated, and include a link to https://webiano.digital and to this original article. Full or substantial republication requires prior written permission. Read our Copyright and Content Use Policy. |