China is no longer treating automated food delivery as a stage trick. In selected cities, Meituan drones already move meals, drinks and daily goods across fixed low-altitude routes, while restaurants, shopping areas and robot-themed venues are testing service robots and humanoids in controlled spaces. The important distinction is clear: drone food delivery in China is already commercial in defined corridors; humanoid food delivery is still early, mostly indoor, promotional or tightly supervised. That split matters more than the viral videos. It shows where automation is working now, where it remains experimental, and why China is using local services as a proving ground for a wider machine economy.

Table of Contents

A delivery experiment that is no longer just a demo

The most useful way to understand China’s automated delivery push is to separate spectacle from infrastructure. A humanoid robot carrying a tray across a restaurant floor makes a better video than a drone route map. Yet the drone route map says more about the future of delivery. It has airspace approvals, launch points, transfer hubs, flight control systems, payload limits, route design, insurance, municipal support and merchant onboarding behind it. A commercial drone delivery network is a system, not a gadget.

Meituan’s drone arm, now branded internationally through Keeta Drone, says it has built a low-altitude drone network since 2017 and can complete three-kilometer deliveries in about 15 minutes. As of March 2026, Keeta Drone said it had launched more than 70 delivery routes across cities including Shenzhen, Beijing, Shanghai, Guangzhou, Hong Kong and Dubai, with more than 880,000 deliveries completed.

That number is still tiny beside China’s daily food-delivery traffic. Meituan’s core business remains built on human couriers, dense merchant coverage and aggressive consumer demand for fast meals, bubble tea, groceries and daily goods. Reuters reported on June 1, 2026, that Meituan’s first-quarter revenue reached 91 billion yuan, while the company posted a third consecutive quarterly loss after a bruising subsidy war in China’s instant retail market.

The automation story sits inside that pressure. A company defending margins in a market where customers expect delivery within an hour has every reason to search for cheaper, more reliable and more controllable fulfillment. Drones do not replace the entire delivery network. They attack specific pain points: water crossings, parks, campuses, hospitals, scenic areas, industrial parks, tourist sites and routes where road delivery is slow, congested or expensive.

Humanoid robots sit at a different stage. They are visible in China’s broader robotics boom, and they have appeared in food-service settings. Beijing’s robot-themed restaurant opened in August 2025 with food-delivery robots, waste-collecting robots and humanoid characters interacting with guests. China Daily also described humanoid robot bartenders, robot bands, delivery robots and machines preparing pancakes, coffee and milk tea at the venue.

That is real deployment, but not the same as a humanoid replacing a rider on a rainy street. A robot that moves inside a mapped restaurant is working in a controlled environment. A courier must cross roads, enter buildings, negotiate elevators, call customers, handle blocked gates, avoid scooters, protect hot food, adapt to last-minute instructions and take responsibility for failure. China is much closer to commercial drone corridors and wheeled delivery robots than to general-purpose humanoid couriers.

The news value is not that every Chinese meal is about to arrive by machine. It is that China is turning the mundane act of ordering lunch into a testing ground for airspace management, embodied AI, urban logistics, machine safety, service robotics, local-government industrial policy and platform economics. Food delivery is the perfect stress test because it is frequent, time-sensitive, low-margin and unforgiving.

The real split between drone delivery and humanoid delivery

The phrase “food delivered by drones and humanoid robots” sounds like one story. It is actually two stories moving at different speeds.

Drone delivery has a narrow but mature logic. A package is loaded at a launch point, flown along an approved route, dropped at a kiosk or handoff point, then collected by a customer or a ground worker. The route is constrained. The payload is limited. The transfer points are known. Weather, battery state, dispatch timing and airspace permissions are monitored. This is why drone delivery can scale route by route.

Humanoid delivery has a wider but less mature ambition. A humanoid robot is meant to use a body shaped for human environments. In theory, it could open doors, press elevator buttons, carry bags, walk through lobbies and hand items to customers. In practice, those tasks demand reliable locomotion, dexterous manipulation, vision, language understanding, safety controls, battery endurance, remote supervision and liability rules. The shape is familiar; the engineering is brutal.

China’s current market reflects that split. Drones are already performing scheduled commercial delivery in selected urban scenarios. Humanoid robots are being pushed through demos, restaurants, investment rounds, factory pilots, reception work, tour guiding, inspection and experimental logistics. Reuters reported that Unitree’s humanoid industry-application revenue still mainly came from enterprise reception and tour-guide use, intelligent manufacturing and inspection, with tour-guide use accounting for roughly 50 to 70 percent.

Drone delivery in China compared with humanoid food service

| Format | Current maturity in China | Best-fit food use | Main constraint |

|---|---|---|---|

| Delivery drones | Commercial on fixed routes | Parks, campuses, tourist sites, hospitals, cross-water routes | Airspace, weather, payload and handoff points |

| Wheeled delivery robots | Scaling in streets, campuses and compounds | Parcels, groceries, takeout transfer legs | Road permissions, speed and curb access |

| Indoor service robots | Common in restaurants and hotels | Tray delivery, table service, recycling | Crowded interiors and human interaction |

| Humanoid robots | Early pilots and staged service roles | Greeting, demonstration, controlled indoor delivery | Cost, reliability, autonomy and safety |

The table shows the core market distinction: China’s automated delivery is not one technology replacing riders everywhere. It is a mixed system matching different machines to different route problems.

That mixed system explains why some videos exaggerate the present while still pointing toward a real direction. A drone dropping bubble tea at a Shenzhen kiosk is not a full replacement for a rider. A humanoid serving burgers at a robot restaurant is not proof that apartment delivery is solved. Yet both developments matter because they push platforms, regulators and suppliers to solve practical problems around machine movement in public and semi-public space.

The strongest near-term case is not a “robot courier” in the human sense. It is machine-assisted fulfillment. A drone does the air leg. A human or locker handles the final handoff. A wheeled robot moves parcels to a transfer station. A courier completes the last hundred meters. A restaurant robot brings trays from kitchen to table. A humanoid greets customers, demonstrates brand technology or handles a constrained service task.

China’s delivery platforms have an advantage here because they already operate dense networks of merchants, riders, consumers, payment systems, order dispatch tools and customer-service workflows. When automation enters that system, it does not need to invent demand. It needs to fit into existing demand without breaking reliability.

That is why the story is bigger than robots. The platform knows where orders originate, which merchants are dense enough to justify a route, where customers wait, which times produce peaks, which districts support pilots, and where ground delivery is weakest. Data-rich delivery platforms are not just buyers of machines; they are the coordinators that decide where machines become useful.

Meituan’s drones moved from pilots to commercial infrastructure

Meituan’s drone program began long before the current global excitement over humanoids. The company established its drone unit in 2017, delivered its first real UAV order in Shenzhen in early 2021, opened a regular route in Shanghai in December 2022, and has kept expanding through selected city corridors. Yicai reported in May 2026 that Meituan’s drone delivery infrastructure had moved into commercial operation rather than remaining in a test stage.

The infrastructure matters because it shows what a drone delivery service actually requires. Yicai described Meituan’s self-developed M-Drone 4L Winch, M-Port 3 smart transfer hub and M-DaaS 3 drone operations control system. Those names sound technical, but the concept is straightforward. A drone service needs aircraft, ground stations, loading systems, dispatch software, monitoring, route permissions, batteries, maintenance and a way to hand orders to customers without forcing aircraft to land in unsafe places.

Meituan’s fourth-generation drone, unveiled in 2023, was designed for urban delivery and could deliver within a three-kilometer radius in about 15 minutes, according to TechNode’s report on the launch. The model had a maximum delivery distance of 10 kilometers, an increase from the previous generation.

The drone is only one piece. The transfer hub is just as important. A drone cannot land wherever a customer happens to be. Dense cities are full of pedestrians, trees, wires, balconies, traffic lights, uneven rooftops and restricted zones. A smart hub or kiosk gives the aircraft a known point. The customer accepts a small trade-off: walk to the kiosk, get the order faster or more reliably, and let the drone avoid unsafe final-meter behavior.

That compromise is one reason China’s drone model differs from many Western suburban pilots. In the United States, drone delivery is often imagined as a backyard drop or direct-to-home service. In dense Chinese districts, the more practical model is route-based. The machine flies between controlled nodes. Human workers, couriers, lockers or customers handle the last step.

Meituan’s reported order growth shows how route-based delivery can move from a curiosity to a working service. China Daily reported that the company had 53 drone routes in major cities including Shenzhen, Beijing, Shanghai, Guangzhou and Nanjing by the end of 2024, with more than 450,000 completed orders. Yicai later reported that by the end of 2025 Meituan had 70 routes in cities including Shenzhen, Beijing, Shanghai, Guangzhou, Hong Kong and Dubai, with cumulative orders exceeding 780,000. Keeta Drone’s own March 2026 page stated more than 880,000 deliveries.

Those figures should be read carefully. They are evidence of commercial progress, not proof of mass replacement. A platform such as Meituan handles an enormous volume of human-courier orders. Drone orders remain a thin slice. Yet the trajectory is still meaningful because drone delivery depends on a fixed-cost network. Once a site, route, hub and regulatory framework exist, incremental volumes become cheaper to test.

Yicai reported that Meituan’s drone business head Mao Yinian said a single site’s handling capacity had risen from about 10 orders a day to as many as 400, while operating costs per order had been falling by roughly 40 to 50 percent each year as equipment, battery, energy-use and site-rental costs declined.

If that pattern holds, the economic argument changes. Early drone delivery looks expensive because the aircraft and infrastructure are underused. Later drone delivery becomes more plausible when utilization rises, maintenance routines mature, routes multiply and local governments provide clearer support. A drone route is not judged only by today’s order count; it is judged by whether the same corridor can handle food, drinks, medicine, samples, emergency goods and retail items across more hours of the day.

The low-altitude economy gives the drone story political weight

Meituan’s drone program is not happening in a policy vacuum. China has made the “low-altitude economy” a national industrial priority. The term covers economic activities involving manned and unmanned aircraft in low airspace, including delivery drones, inspection aircraft, emergency services and eventually passenger eVTOL services. China’s State Council information portal reported in May 2026 that the Civil Aviation Administration of China had set up a low-altitude safety department to coordinate development plans, safety work, dispatch platforms and flight service station systems.

That institutional move says a lot. A drone food delivery route might look local and small. A national safety department treats the same activity as part of a future transport layer. China’s government portal said the low-altitude economy usually refers to manned and unmanned aerial vehicles operating within 1,000 meters above ground and that the market size is expected to exceed 3.5 trillion yuan by 2035, according to the CAAC.

Policy support does not remove the hard parts. It can reduce uncertainty. Cities can designate routes, coordinate local agencies, support takeoff and landing sites, test flight-service systems, allow commercial pilots and attract manufacturers. Without public-sector cooperation, urban drone delivery struggles to escape demonstration status. With too much enthusiasm and too little discipline, cities risk duplicating infrastructure that never earns its cost.

Reuters captured that tension in August 2024, reporting that China’s low-altitude economy had drawn investor interest but still lacked a clear development roadmap, according to the China Low Altitude Economic Alliance. The same Reuters report said China’s aviation regulator foresaw a 2-trillion-yuan industry by 2030, while industry voices warned that many companies were enthusiastic but confused about the business model.

That warning is still relevant. A national industrial push can create real capacity. It can also create a rush of local pilots searching for subsidies, media attention or land-use justification. Drone delivery will not scale simply because “low-altitude economy” appears in policy documents. It scales when enough routes produce repeat demand, safe operations, low complaint rates and acceptable economics.

The 2024 Implementation Plan for Innovative Application of General Aviation Equipment, jointly issued by MIIT, the Ministry of Science and Technology, the Ministry of Finance and CAAC, put logistics distribution among the target fields for new unmanned, electrified and intelligent general aviation equipment. The plan aimed for commercial application in fields including urban air transportation, logistics distribution and emergency rescue by 2027, with a stronger low-altitude economic model by 2030.

That policy timeline fits Meituan’s commercial timeline. The company spent years building aircraft, hubs and route experience before the national conversation reached its current intensity. China’s food-delivery drones are now both a logistics experiment and a political demonstration of low-altitude industry. They show officials that low-altitude airspace can produce visible consumer services, not just industrial inspection or emergency response.

The risk is that visibility can distort judgment. A drone delivering coffee to a park is easy to film. The hard value may come from less photogenic uses: medical samples, laboratory logistics, supplies to areas cut off by terrain, emergency goods in heat waves, or short crossings where road routes are slow. Meituan itself has pointed to medical sample routes in Shanghai and Sichuan as part of its low-altitude delivery use cases.

The Shenzhen model built around kiosks, ports and fixed corridors

Shenzhen is the natural home of China’s drone delivery story. The city has dense consumer demand, deep hardware supply chains, strong municipal interest in the low-altitude economy, and a reputation for accepting urban technology pilots. It is also close to the manufacturing networks that make drones, sensors, batteries and automation equipment cheaper to iterate.

Meituan’s early real-order delivery took place in Shenzhen in 2021, and the city has remained one of the company’s core drone markets. Keeta Drone lists Shenzhen examples such as Futian Port and Talent Park among its business footprints.

The Shenzhen model is not magic. It is a logistics design. Dense order clusters give drones enough demand. Parks, ports, scenic areas and campuses create controlled destination points. Merchants can be grouped around takeoff locations. Customers can be trained to collect from cabinets or kiosks. Local authorities can make airspace coordination more predictable than it would be in a fragmented jurisdiction.

That matters because drone delivery fails when every order is unique. A rider can improvise. A drone network needs repeatable geometry. The best early drone routes have the feel of invisible conveyor belts. They move small goods between known points over obstacles that slow ground transport. They do not try to solve every address.

A drone carrying lunch across a park has no traffic lights, no delivery elevator, no illegal parking problem and no flooded sidewalk. It still has battery limits, wind exposure, payload constraints and safety obligations. The question is whether the route removes enough ground friction to justify the air system.

Shenzhen also illustrates why drone delivery is likely to be intermodal. A merchant prepares an order. A worker or courier brings it to a drone hub. The drone flies to a destination hub. A consumer, staff member or courier completes pickup. The drone is the fast middle leg, not the entire service. That model may sound less futuristic than doorstep aircraft, but it is much more plausible in dense cities.

The same logic applies to border checkpoints and ports. A controlled point such as Futian Port has predictable flows, constrained geography and intense demand for quick handoffs. Drones can serve these nodes without needing to fly randomly through apartment clusters.

This is why Meituan’s network details are more important than drone specifications alone. A better battery matters. A quieter propeller matters. Yet the breakthrough is often operational: where to place hubs, how to batch orders, how to schedule flights, how to handle rain, how to keep food warm, how to verify pickup, how to coordinate with human couriers and how to respond when a customer is late.

Shenzhen gives China something many markets lack: a high-density urban laboratory where hardware makers, platforms and local authorities can repeatedly adjust the same service. That repetition is the hidden force behind commercialization.

Shanghai shows the urban park use case

Shanghai’s Yangpu district offers a clean example of where drone food delivery makes immediate sense. In July 2024, Shanghai’s official English government site reported that Meituan had launched a UAV delivery service allowing customers to order food, beverages and essentials from the Wujiaochang commercial area, with goods transported to a designated station in Huangxing Park and delivery times cut to as little as 10 minutes. Participating merchants included Starbucks, Chagee and Yang’s Dumpling.

This is exactly the kind of scenario where drones have a rational role. Parks can be large. Walking out to a commercial area takes time. Conventional couriers may face entry rules, traffic bottlenecks or long detours. Customers are not asking for complex doorstep service. They are gathered in a public space and can collect at a fixed station.

Shanghai’s report also said that by the end of June 2024 Meituan’s UAV service had established 31 air delivery routes in key cities such as Shanghai, Shenzhen and Guangzhou, completing more than 300,000 orders and covering offices, residential communities, tourist spots, municipal parks, healthcare facilities, campuses and libraries, with more than 90,000 products available.

That mix of sites is telling. A library, park, hospital and campus are not the same. They share a need for controlled access and concentrated foot traffic. They also tend to have enough order density to justify a pickup point. The model is not “drones everywhere.” It is “drones where a route can repeat.”

Shanghai also shows why municipal support is central. The Yangpu district official quoted in the report linked the service to policy support, technological application, logistics distribution and urban governance.

A private company can build drones. A city decides whether those drones fit public space. That means drone delivery in China is partly a municipal governance product. It must answer questions that a normal delivery app can often avoid: Who manages the landing point? Who handles complaints? What happens if a drone fails? How are routes marked? How does the service coexist with parks, hospitals and schools? Who approves nighttime or rain operations?

Those questions are mundane. They are also the difference between demonstration and infrastructure. Shanghai’s urban park model works because it reduces uncertainty. A customer in a park can walk to a station. A drone can fly to a station. The merchant and platform can build a repeatable process. The city can monitor a defined use case.

This is why drone delivery may expand less like ride-hailing and more like rail transit, bike-share docks or parcel lockers. It grows through nodes. The nodes then become habits. Once customers know that a certain park, campus or hospital has an aerial delivery point, orders become less theatrical.

The future of China’s drone delivery may depend less on the aircraft flying above people and more on the small pickup points people learn to use without thinking.

Beijing’s Great Wall route explains the niche value

The Great Wall drone route, launched by Meituan at Badaling in 2024, became internationally visible because it looked dramatic: tourists at a remote section receiving food, drinks and supplies from the sky. Yet its importance is not the novelty. It is the use case.

A scenic area has a clear delivery problem. Visitors spread across terrain. Commercial facilities may be limited or restricted. Heat, fatigue and emergency needs matter. A walking route that takes nearly an hour can be shortened by air. New York Post, summarizing the launch, reported that Meituan’s route delivered food, drinks and medical supplies to a watchtower on the southern extension of Badaling, reducing a trip that could take 50 minutes on foot to about five minutes by drone, with a delivery fee matching the regular Meituan fee of 4 yuan.

A tourist site also solves some customer-behavior problems. People are already moving to designated points. They accept that not every service reaches them directly. They may value emergency supplies and drinks more than doorstep convenience. The drone’s value is obvious because the ground alternative is visibly slow.

This is the sort of niche where drone delivery can feel less like a gimmick. It solves a physical geography problem. The same logic could apply to islands, river crossings, campuses split by roads, hospitals with multiple buildings, industrial parks, ports and large parks. In each case, the drone is not competing with a courier walking down a normal street. It is bypassing a route penalty.

Tourist-site delivery also introduces a second role: waste removal. Reports on the Badaling route said drones could carry trash after order service hours. That matters because low-altitude logistics can serve two-way flows. A drone that brings supplies in and takes waste out has better utilization than a drone that returns empty.

The Great Wall route does not prove that urban drone delivery is ready everywhere. It proves something narrower and more useful: where distance, terrain, safety or visitor welfare create enough friction, a small-payload drone can deliver clear value.

For platforms, such routes create public familiarity. A tourist who sees a drone delivery at a scenic site may trust the same platform’s drone pickup station in a park. Familiarity lowers the psychological barrier. The first time a drone lands near a customer, it feels strange. The tenth time, it becomes another delivery option.

For regulators, scenic routes test safety protocols in semi-controlled public space. For merchants, they extend reach without opening new storefronts. For cities, they create a visible low-altitude economy application that can be described to citizens and investors. For the platform, they generate operational data under real consumer demand.

Still, scenic routes are not the core market. They are proof points. The larger market sits in repetitive, high-density urban logistics. A Great Wall route explains why drones are useful. The city network decides whether they are economically material.

Drone logistics works best where ground couriers lose time

The strongest economic case for drone delivery is not speed in isolation. It is speed where ground delivery is inefficient. A scooter courier is already fast in many Chinese neighborhoods. Replacing that courier with an aircraft only makes sense when the courier’s route is distorted by geography, access rules, congestion or distance.

Food delivery has a hard timing structure. Customers care about temperature, freshness and predictability. Platforms care about dispatch density, courier utilization and failure rates. Merchants care about whether the meal arrives in good condition and whether the platform brings incremental orders. A drone route must improve at least one of these variables enough to offset hardware and infrastructure costs.

The best-fit zones share several traits. They have clustered demand. They have a clear origin-destination pattern. They have limited direct road access. They allow fixed receiving points. They involve small payloads. They produce repeat orders across the day. They are acceptable to local regulators and the public.

This is why drinks are a natural category. Bubble tea, coffee and bottled beverages are small, frequent, branded and often ordered from dense merchant clusters. They can be packaged consistently. They do not require the same delicacy as soup noodles or fragile plated dishes. They create repeat habits.

Medicine and medical samples add another layer. They may justify higher urgency than ordinary meals. Yicai reported that Meituan’s low-altitude services include medical sample routes in Shanghai and Sichuan province, with urgent supplies sent directly to designated points.

Food and medicine may seem like different businesses, but they share a dispatch logic: small items, high time sensitivity, and value in bypassing road friction. Once a drone corridor exists, the platform can test categories. A lunch route may carry drinks at noon, medicine in the afternoon and emergency supplies during a heat wave.

The aircraft does not need to be large. In fact, small payloads are a feature. Urban drone delivery works better when vehicles are light enough to reduce risk, noise and energy use. The payload ceiling shapes the product mix. A drone carrying two coffees and a snack is more realistic than a drone carrying family groceries.

The trade-off is batching. A courier can carry multiple orders and adjust the route. A drone may carry fewer items per flight, depending on design. Route economics depend on flight frequency, turnaround time, loading labor, battery swaps and demand density. If a site only handles a few orders a day, the infrastructure sits idle. If it handles hundreds, the economics start to change.

This is why Meituan’s reported site-level growth matters. A site moving from 10 orders a day to hundreds suggests the company is learning where demand is thick enough and how to raise throughput.

The right question is not whether drones are faster than people. Sometimes they are, sometimes they are not. The right question is which route segments are expensive for humans and simple for aircraft. China’s current pilots are gradually answering that question with commercial data.

The hidden labor still inside automated delivery

Automated delivery is often presented as a machine replacing a worker. In the near term, China’s drone and robot delivery systems show something different: machines rearrange labor before they remove it.

A drone order still involves people. A merchant prepares the item. A worker may package it for flight. A staff member may load it into a drone hub. A remote operations team supervises flights. Maintenance crews inspect aircraft and batteries. A worker or customer may collect at the destination. Customer-service agents handle exceptions. Regulators and platform safety teams monitor compliance.

The same is true for wheeled robots. A vehicle may drive itself along a street or campus, but humans still load compartments, clear stuck vehicles, manage permits, maintain sensors, clean units, repair doors, respond to blocked routes and handle customers who fail to collect orders.

Humanoid robots add even more hidden labor. Many humanoid systems still rely on teleoperation, scripted routines, pre-mapped spaces or human trainers. A humanoid in a restaurant may greet guests, deliver a tray or perform a programmed interaction, but staff remain close. The service works because the environment is designed around the robot’s limits.

This hidden labor matters for two reasons. First, it keeps claims honest. An automated delivery service is not workerless just because the middle leg is handled by a drone or robot. Second, it shows where new jobs appear: drone dispatchers, robot fleet technicians, data collectors, safety monitors, route planners, maintenance staff and local operations managers.

China’s delivery sector has millions of workers tied to platforms, couriers, merchants and logistics firms. Automation does not land in a clean spreadsheet. It lands in a labor market with wages, social insurance debates, safety concerns, algorithmic management and intense competition. Reuters reported in 2025 that Meituan planned to provide social security benefits to delivery riders starting in the second quarter of 2025, amid competition and public attention to rider welfare.

That labor context shapes automation. Platforms want lower unit costs and greater reliability, but they cannot simply remove riders from a city network without damaging coverage. Human couriers provide flexibility that machines lack. They handle unclear addresses, customer calls, weather, traffic improvisation and merchant delays. They are also the face of service recovery when something goes wrong.

Machines are likely to take the repeatable legs first. A drone handles a fixed crossing. A wheeled robot moves goods from a sorting point to a community transfer station. A service robot moves trays across a restaurant. A humanoid performs greeting or demonstration tasks. Riders then focus on final handoff, exceptions, peak demand and complex addresses.

This can improve some courier work if it removes dull transfer legs and raises delivery density. It can also increase monitoring and pressure if platforms use automation to reset productivity expectations. People’s Daily reported that Meituan’s hybrid model in Beijing’s Shunyi district uses unmanned vehicles to move parcels to transfer stations, with couriers completing the last hundred meters, and quoted Meituan’s unmanned vehicle division as saying couriers’ average monthly deliveries and earnings had risen.

That is the platform-friendly version. The worker reality will vary. A courier who gets more local drop-offs may earn more. A courier whose route is hollowed out by drones may lose volume. A technician role may pay better but require new skills. The labor story is not disappearance; it is redistribution.

Unit economics and the pressure on food delivery platforms

China’s automated delivery push cannot be separated from the economics of food delivery. Food delivery is a brutal business: low ticket sizes, peak-time surges, merchant commissions, consumer subsidies, rider costs, customer-service failures, weather shocks and intense local competition. Automation is appealing because it promises more control over cost and capacity. It also demands heavy upfront investment.

Reuters reported on June 1, 2026, that Meituan posted a third consecutive quarterly loss while revenue grew 5.6 percent year on year to 91 billion yuan. The report tied pressure to a subsidy-fueled battle in China’s one-hour delivery space after Alibaba’s Taobao and JD.com launched instant retail platforms in early 2025.

This is the business background for drones and robots. When platforms compete through subsidies, margins suffer. When regulators criticize price wars, platforms need to compete through service quality, merchant selection, delivery reliability and operational efficiency. Automation becomes a way to signal future efficiency even before it changes the income statement.

But the economics are not automatic. A drone route has aircraft costs, batteries, maintenance, insurance, hub rent, loading labor, software, safety monitoring and regulatory compliance. A humanoid robot has even higher hardware cost, shorter useful-task range and more uncertain maintenance. If order density is weak, the machine is a marketing expense.

The strongest case for drones is where they reduce costly courier time. A rider spending 20 minutes on a detour across a park or around a river is a poor use of human capacity. A drone flying a straight line can reduce that waste. The rider can stay in a dense neighborhood. The platform may improve throughput without hiring more riders for peak demand.

The strongest case for wheeled robots is repetitive local transfer. A small autonomous vehicle moving parcels from a depot to a community point does not need to charm customers. It needs to follow a route, stop safely and unlock compartments. People’s Daily reported that more than 6,000 autonomous delivery vehicles were in operation across China by the end of 2024 and that by mid-2025 more than 100 Chinese cities had opened roads to unmanned delivery vehicles.

The strongest case for humanoids is not yet food delivery at scale. It is data collection, brand demonstration, reception, simple indoor service, factory logistics and eventually tasks in human-designed spaces where a wheeled robot struggles. Reuters reported that Unitree’s humanoid revenue mix remained concentrated in reception, tour-guide, manufacturing and inspection scenarios rather than general consumer delivery.

A platform such as Meituan can afford to test all three layers because it has large order flow. A smaller delivery firm cannot. This creates a scale advantage. The platform with the most demand can better identify profitable routes, keep hubs busy, negotiate with cities, invest in hardware suppliers and collect operational data. Automation may strengthen the largest platforms because the machines work best where order density is already high.

That could create regulatory tension. China’s authorities have already shown concern over “involution”-style price wars and platform food safety. Reuters reported that regulators criticized the instant retail battle as a “race to the bottom,” and that China’s market regulator fined seven e-commerce platforms, including Meituan, over food delivery safety violations in April 2026.

Automation may solve some safety problems, but it introduces others: airspace incidents, battery fires, sidewalk obstruction, data security, liability, and public discomfort with machines in shared spaces. The unit economics will only matter if the safety economics hold.

Price wars pushed automation from curiosity to strategic hedge

The Chinese food-delivery market entered a new phase when instant retail became a battlefield among Meituan, Alibaba and JD.com. Instant retail means goods ordered online and delivered within about 60 minutes, often through local stores and food-delivery-style networks. Reuters described it as purchases of food, bubble tea and daily-use items delivered within 60 minutes.

Alibaba’s Taobao Instant Commerce passed 40 million daily orders within a month of launch in 2025, according to Reuters. That development intensified pressure on Meituan because Alibaba could combine Taobao traffic with Ele.me’s local delivery base. JD.com brought its logistics reputation and supply-chain strength into the same field.

In that environment, drones and robots become more than experiments. They are strategic hedges. A platform does not know exactly which delivery mode will produce the best economics five years later. It does know that relying only on human couriers exposes it to wage pressure, social insurance costs, weather disruptions, rider churn and regulatory scrutiny. A mixed fleet gives optionality.

This is why Meituan’s investments in drones, autonomous vehicles and humanoid-related startups should be read together. The company is not betting that a humanoid will deliver every lunch next year. It is building exposure to the physical automation stack: aerial delivery, ground autonomy, embodied AI, robotics hardware, control systems, data and service integration.

Yicai reported in July 2025 that the competition between JD.com and Meituan had spilled into the humanoid robot market, with JD.com investing in Spirit AI, Engine AI and LimX Dynamics, while Meituan had participated in multiple humanoid-related fundraisers, including Galaxea, TARS and X2 Robot.

This investment race does not mean food delivery platforms suddenly became robot manufacturers. It means they want a seat near the supply chain. The platform with real delivery scenarios can offer robotics startups something valuable: messy operational problems. A robot company needs places to test navigation, manipulation, charging, dispatch, customer interaction and maintenance. A delivery platform has millions of such problems.

The pressure also comes from investor narrative. When margins are hit by subsidies, investors look for evidence that the company has a path back to operational discipline. Automation gives management a way to argue that the long-term delivery network will be more efficient than the current rider-heavy model. It does not guarantee that outcome, but it creates a plausible story.

The danger is overpromising. A company can spend heavily on robots while losing money in its core market. Shareholders may tolerate that if they believe automation will create a moat. They may punish it if drones remain too small and humanoids remain theatrical. The difference between strategic hedge and expensive distraction will be measured in route economics, not demo quality.

China’s platform war also affects merchants. A café or dumpling shop may welcome drone delivery if it reaches park customers in 10 minutes. It may not welcome another platform program that requires packaging changes, operational complexity or discounts. Automation must fit merchant workflows. A drone route that forces a restaurant to assign staff to special loading without enough order volume can become a burden.

The platforms know this. Their advantage lies in bundling demand across many merchants. A drone hub near a commercial district can aggregate coffee, tea, snacks, medicine and convenience goods. It does not depend on one restaurant. That aggregation is why instant retail and drone delivery are linked. The machine serves the local commerce cloud, not a single menu.

Ground robots are scaling faster than humanoids

Ground delivery robots are less glamorous than humanoids and less dramatic than drones, but they may scale faster in everyday logistics. They are cheaper, simpler and better matched to parcel and grocery transfer. They do not need legs, hands or humanlike balance. They need reliable sensors, safe low-speed driving, compartments, route permissions and fleet management.

China already has meaningful deployment of autonomous delivery vehicles. People’s Daily reported that more than 6,000 autonomous delivery vehicles were operating across China by the end of 2024. The report described uses by express-delivery firms and a Meituan hybrid model in Beijing’s Shunyi district, where unmanned vehicles transport parcels to transfer stations and couriers complete the last hundred meters.

JD Logistics has also used delivery robots for years. Its corporate blog reported that during Singles’ Day 2022 it operated 600 autonomous outdoor delivery robots and 100 indoor delivery robots in China, with some Sam’s Club and SEVEN FRESH stores using the system for on-demand omni-channel orders. JD said its delivery robots could carry up to 200 kilograms and travel 100 kilometers per charge.

Those numbers are older than the current humanoid hype, which is precisely the point. Wheeled robots have had time to mature because the task is clearer. A box on wheels can carry parcels better than a humanoid in most outdoor delivery scenarios. Legs are useful for stairs, clutter and human-shaped environments, but they add cost and risk. Roads, campuses and compounds reward wheels.

For food delivery, wheeled robots work best in bounded spaces: campuses, office parks, residential compounds, industrial parks, hospitals, airports, shopping centers and planned districts. They can move slowly without blocking fast traffic. Customers can collect from compartments. Security rules can be standardized. Maintenance teams can reach stuck units quickly.

Humanoids may eventually work in those spaces too, but they must justify their extra complexity. If a robot only needs to move a sealed meal from a lobby to a pickup shelf, wheels win. If it needs to open doors, press lift buttons, navigate narrow corridors and hand the bag to a person, a humanoid becomes more relevant. The trouble is that every extra humanlike task introduces failure modes.

This is why China’s near-term automated food-delivery system is likely to contain many non-humanoid robots. A “robot delivery” headline may refer to a sidewalk vehicle, indoor tray robot, hotel service robot or autonomous van. Humanoids will be present, but they will not dominate practical last-mile movement soon.

The public may not care about the technical distinction. To a customer, the order arrived by robot. To operators, the distinction decides cost, safety and uptime. A wheeled robot’s lower center of gravity, larger battery space and simpler controls make it easier to manage. A humanoid’s expressive body, arms and ability to use human tools make it more flexible but less mature.

China’s robot delivery future will probably be less human-shaped than the marketing suggests. The most common machines may be drones in the air, boxy autonomous vehicles on the ground and service carts indoors. Humanoids will appear where their body form creates value or brand attention.

Humanoid robots are entering food service through the dining room

The dining room is a safer place for humanoid robots than the street. It is mapped, supervised and commercially useful even when the robot performs a limited role. Restaurants can use humanoids for greeting, entertainment, education, brand storytelling, table interaction and simple service. These tasks do not require full courier autonomy.

Beijing’s robot-themed restaurant shows the pattern. The official Beijing government site said the venue opened on August 8, 2025, near Robot World in the Beijing Economic-Technological Development Zone, with more than 20 robotics models, human-robot interaction, smart navigation and dining services. It described food-delivery robots and waste-collecting robots moving through the dining area, while humanoid robots named after Chinese poets interacted with guests.

China Daily’s report on the same venue described humanoid robot bartenders, robot musicians, robot comedy, delivery and recycling robots, and machines preparing pancakes, coffee and milk tea. It also connected the opening to the World Robot Conference and the World Humanoid Robot Games, which brought more than 500 humanoid robots from around the world to compete in Beijing.

Hangzhou added another example. Global Times reported in February 2026 that an AI-powered robot restaurant in Hangzhou replaced traditional chefs with robots that stir-fry, boil noodles, brew coffee, make ice cream, deliver dishes and clean the floor.

These restaurants should not be dismissed as mere gimmicks. They are commercial labs. Customers provide feedback. Operators learn where robots slow service. Engineers observe failures in navigation, interaction and cleaning. Cities display local robotics ecosystems. Platforms such as Meituan and Dianping can make bookings and consumer response visible.

Yet robot restaurants are not proof of general-purpose autonomy. They are designed around robots. The floor plan, menu, traffic flow and staff behavior can be adjusted to fit machine limits. That is the opposite of a normal apartment delivery route, where the world refuses to cooperate.

A humanoid in a restaurant may succeed by doing less. It may greet customers, explain dishes, perform a cultural routine or carry lightweight items over short distances. It does not need to solve every object, every door or every weather condition. The business case is partly service and partly theater.

The theater is not useless. Consumer acceptance matters. Robots entering public life need a period of social adjustment. A diner who watches a robot deliver a dish may become less surprised by a robot in a hotel, hospital or shopping center. A child who sees a humanoid at a restaurant may grow up treating such machines as normal. Public familiarity reduces friction for later deployments.

There is still a risk of confusion. Media clips of humanoids serving meals can make it seem that China has solved robotic labor. It has not. It has built enough capability to stage and operate narrow service tasks. The difficult work remains reliability under messy conditions. For food service, the strongest near-term use may be hybrid: robots handle repeated indoor movements, while humans manage hospitality, exceptions and quality.

Robot restaurants are marketing labs, not proof of street autonomy

A robot restaurant is valuable because it condenses many service tasks into a controlled space. It is not valuable because it proves a humanoid can work as a city courier. The distinction should be kept sharp.

Street delivery has an open-world problem. The robot faces unpredictable surfaces, cyclists, pets, children, blocked sidewalks, construction barriers, traffic rules, weather and social behavior. A restaurant has a managed-world problem. The robot faces known tables, staff corridors, pre-defined stopping points and customers who expect the robot to behave oddly.

Humanoid robots are especially sensitive to this difference. Legs give them access to stairs and human-designed spaces, but legs also create stability, energy and safety issues. A falling humanoid is not just a failed delivery. It is a public hazard. Arms make handoff possible, but arms also create pinch points, collision risks and liability questions. Faces and voices make interaction easier, but they raise privacy and emotional-design concerns.

This is why many restaurant robots are not humanoid. Pudu Robotics’ BellaBot, for example, is a cat-like smart delivery robot with multi-modal interaction designed for food delivery experiences, according to the company’s product page. It uses a practical wheeled form because carrying trays across a restaurant does not require human legs.

Restaurant operators care about turnover, labor allocation, novelty, cleaning, customer wait time and order accuracy. A wheeled tray robot may free human staff from walking the same route repeatedly. It may also create bottlenecks if customers block it, children chase it or staff must intervene too often. The business case depends on layout and volume.

Humanoids add brand value. A humanoid bartender or greeter draws attention. A robot based on Li Bai or Su Shi creates cultural entertainment. A humanoid explaining cooking science turns a meal into a technology exhibition. That can generate foot traffic and social media reach, especially around events such as the World Robot Conference.

The danger is that restaurants become misleading showcases. The public sees a humanoid speaking in a dining room and assumes it understands the world. In many cases, the behavior may be scripted, remotely supervised, constrained or dependent on pre-mapped conditions. That does not make it fake. It makes it early.

The honest reading is that China is using food service as a bridge between industrial robotics and public-facing embodied AI. Restaurants are one of the few spaces where people will pay to interact with robots even when the robots are imperfect. That gives companies data, revenue and attention while the technology matures.

The same bridge may extend to hotels, hospitals, eldercare centers, malls, museums and airports. These environments are more predictable than streets and more service-oriented than factories. A humanoid that is not yet ready to replace a courier may still greet visitors, carry light objects, guide people, collect dishes, clean surfaces or assist staff.

This is why humanoid food delivery should be described with care. China has humanoid robots in food-service settings. It has restaurant delivery robots. It has drone food delivery. It does not yet have broad, unsupervised humanoid courier delivery across ordinary city streets. The market is heading toward embodied service automation, but the body forms and use cases remain unsettled.

The JD and Meituan robot investment race

JD.com and Meituan are not robotics companies in the narrow sense. They are demand owners. They control flows of orders, merchants, warehouses, couriers, customers and payment data. That makes them powerful partners for robotics firms looking for real-world deployment.

Yicai reported in July 2025 that JD.com and Meituan extended their food-delivery rivalry into the humanoid robot market. JD.com led or joined funding rounds for Spirit AI, Engine AI and LimX Dynamics, while Meituan participated in several humanoid-related fundraisers, including Galaxea, TARS and X2 Robot, and had invested in Unitree Robotics.

This investment activity should be read as positioning. Both companies are trying to avoid being locked out of a future delivery stack. If humanoids become useful in logistics, retail or service, the platform that has already built relationships with leading robot makers will move faster. If humanoids disappoint, the same investments may still yield technology for perception, manipulation, fleet management or factory automation.

JD’s logic differs from Meituan’s. JD has a deep logistics infrastructure built around warehouses, supply chains and parcel movement. Its delivery robots and autonomous vehicles fit that heritage. Meituan’s strength is local life services: meals, groceries, shops, restaurants, hotels and instant retail. Its automation focus naturally leans toward urban fulfillment, drone routes, merchant density and consumer pickup points.

The rivalry is practical. A food-delivery platform that controls local demand can turn a robot from a demo into a service. A robot maker needs data from repeated tasks. The platform can say: here are 50 campuses, 200 malls, 1,000 restaurants, 10,000 courier handoff points and millions of orders. Try the robot here. Fail here. Improve here.

This is where China has a structural advantage. Many robot firms elsewhere struggle to find dense deployment scenarios. China’s platforms operate in cities where consumers already expect rapid digital services. The gap between online order and physical delivery is small enough to experiment repeatedly.

Investments also act as intelligence gathering. A platform does not need to know which startup will win. By investing across several companies, it watches progress in locomotion, hands, embodied models, manufacturing cost, reliability and customer acceptance. It learns how quickly hardware prices fall and which tasks robots can actually perform.

That learning can shape internal strategy. If humanoids remain expensive, platforms double down on drones and wheeled vehicles. If robot hands improve quickly, they test warehouse sorting, kitchen handling or retail shelf work. If embodied AI models become reliable in semi-structured environments, they introduce robots into malls, hospitals and hotels before streets.

The investment race is not a declaration that humanoid couriers are ready. It is insurance against a future in which physical AI becomes part of the delivery cost structure.

The risk is capital misallocation. Humanoid startups are expensive, technically uncertain and prone to hype. A delivery platform facing margin pressure may look bold for investing in robots, but investors will eventually ask whether those bets lower fulfillment costs. The answer will take years.

China’s humanoid standards turn demos into industrial policy

China’s humanoid robot sector is no longer just a startup scene. It is being pulled into national standard-setting, supply-chain coordination and industrial policy. Xinhua reported in March 2026 that China had unveiled its first national standard system for humanoid robotics and embodied intelligence, covering the entire industrial chain and lifecycle.

The standard system aims to reduce coordination costs, promote modular components, break compatibility barriers, and establish application standards for specific scenarios, including function, adaptation and safety specifications. Xinhua also reported that safety and ethical issues were included in the framework.

This is not just bureaucracy. Standards matter when a sector moves from demos to deployment. If every robot has unique interfaces, sensors, safety protocols, batteries and software tools, large-scale adoption becomes difficult. Restaurants, warehouses, factories and delivery platforms do not want one-off machines that require custom support forever. They want maintainable fleets.

Xinhua reported that 2025 was considered China’s first year of humanoid robot mass production, with more than 140 domestic manufacturers releasing over 330 models within 12 months, according to MIIT. It also noted challenges such as scenario fragmentation, high costs, weak generalization in AI models and reliance on imported core components.

Those challenges are directly relevant to food delivery. Scenario fragmentation is the enemy of courier replacement. Every apartment block, restaurant, lobby and street corner differs. A humanoid cannot be commercially useful if it needs custom engineering for every building. It needs reusable capabilities: carry, navigate, wait, hand off, recharge, avoid people, understand instructions and recover from mistakes.

Standards cannot create intelligence by decree. They can reduce friction around testing, certification, interfaces, data formats and safety expectations. That allows companies to compare systems more fairly and deploy them with less bespoke work.

China’s approach also links humanoids to broader embodied AI. A robot body needs a “brain” for perception and planning, a “cerebellum” for motion control, and limbs that can act in the world. MIIT’s earlier humanoid guidance emphasized breakthroughs in these areas, with a preliminary innovation system by 2025 and stronger industrial capability by 2027. China’s State Council Information Office reported in 2023 that China aimed to establish a preliminary innovation system for humanoid robots by 2025.

Food delivery is a good test of embodied AI because it combines language, navigation, manipulation and timing. The customer says the gate code changed. The elevator is full. The bag is hot. The soup must stay upright. The robot must wait without blocking people. A drone avoids some of those problems by using fixed stations. A humanoid must eventually face them.

The standard-setting push tells us that China wants humanoid robots to become an industry, not a collection of viral clips. Food service will be one of the public stages where that ambition is tested.

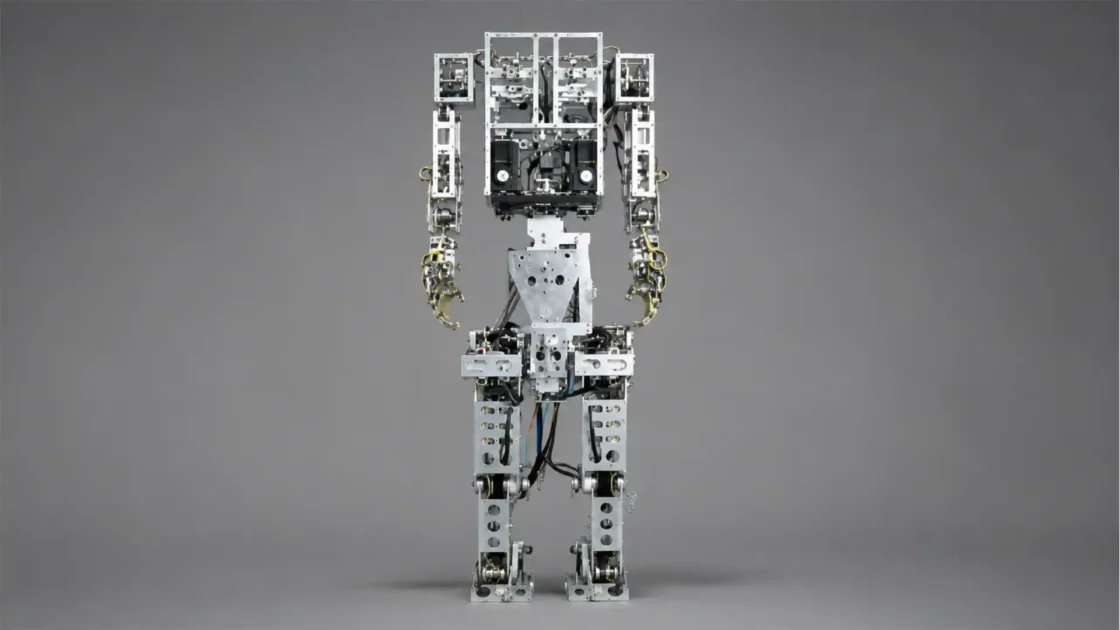

Unitree shows why humanoids are suddenly investable

Unitree Robotics has become a symbol of China’s humanoid momentum because it combines public visibility, relatively low-cost hardware and capital-market ambition. Reuters reported in March 2026 that Unitree filed an application for a Shanghai Stock Exchange IPO seeking to raise 4.2 billion yuan, in what would be one of China’s biggest domestic tech listings in years.

The company’s numbers explain investor interest. Reuters, citing Unitree’s prospectus, reported that operating income grew 335 percent year on year in 2025 to 1.708 billion yuan, while net profit rose 674 percent. Humanoids became the firm’s main growth engine, rising to 51.5 percent of main business revenue in January to September 2025 from 27.6 percent in 2024. Unitree shipped more than 5,500 units in 2025, giving it 32.4 percent of the global humanoid market, according to the prospectus.

Those are striking figures, but the use cases are still early. Reuters also reported that real-world factory deployment remains limited and that Unitree’s humanoid industry-application revenue mainly came from enterprise reception and tour-guide use, intelligent manufacturing and inspection.

That contrast is the humanoid market in miniature. Hardware is advancing quickly. Shipments are rising. Public attention is high. Practical deployment remains narrow. For food delivery, that means humanoids may appear in restaurants, malls and brand spaces long before they become routine couriers.

Unitree’s role also became globally relevant through Nvidia. Reuters reported on June 1, 2026, that Nvidia plans to work with humanoid robot makers in the United States, Europe and South Korea in addition to China’s Unitree, and that Nvidia announced work with Unitree on a standardized H2 robot for academic researchers, with the body from Unitree, hands from Sharpa and computing from Nvidia.

That partnership points to the next phase of humanoid development: reference designs, research platforms, security architecture and standardized computing. The food-delivery implication is indirect but important. Better research platforms may speed progress in navigation, manipulation and real-world learning. They may also raise security concerns because robots in public spaces carry sensors, maps and network connections.

Humanoid robots are machines of trust as much as machines of motion. A delivery robot entering a building may see hallways, faces, door numbers and customer behavior. A humanoid working in a restaurant may record speech and movement. Nvidia’s discussion of secure boot and confidential computing for research robots shows that cybersecurity is not an afterthought.

China’s advantage in humanoids comes from hardware supply chains, manufacturing experience, electric-motor ecosystems, batteries, sensors and a large domestic market for pilots. Its challenge is turning affordable hardware into dependable autonomy. A cheap robot that fails too often is expensive to operate. A reliable robot that costs too much is hard to deploy.

Unitree proves that humanoid robots are entering commercial volume. It does not prove that humanoid food delivery is ready for ordinary streets. The gap between shipment and useful labor remains the central question.

The technical gap between carrying a tray and replacing a courier

A restaurant tray robot solves a narrow problem. A humanoid courier solves a stack of problems at once. That gap is why food delivery is such a difficult robotics benchmark.

A courier’s job looks simple because humans hide the complexity. A person leaves a restaurant, checks the route, avoids obstacles, rides through traffic, finds the right entrance, speaks to guards, uses an elevator, calls a customer, waits, handles a wrong address and adjusts when the customer changes plans. Each step requires perception, judgment and social negotiation.

A drone route removes many of those steps by changing the problem. It uses fixed endpoints and avoids street-level chaos. A wheeled robot removes some steps by operating slowly in mapped spaces. A humanoid takes the hardest path: it tries to work inside human environments without changing them too much.

The robot must localize itself. It must recognize walkable surfaces. It must predict human movement. It must avoid collisions. It must handle doors, stairs or elevators. It must manage payload balance. It must understand instructions from customers and staff. It must know when to ask for help. It must recover safely when it cannot proceed.

Research is moving toward such abilities. A 2025 arXiv paper titled “Hand-Eye Autonomous Delivery” proposed a framework for humanoids to learn navigation, locomotion and reaching skills from human motion and vision perception data, showing real-world experiments in complex environments designed for humans.

That research is promising because it targets the correct problem: a delivery humanoid needs eyes, hands and whole-body movement to work together. The robot must not only walk to a point; it must position itself so it can reach, carry and hand over an item. The food-delivery task is hand-eye coordination wrapped inside logistics.

Drones face their own technical constraints. They must manage weather, wind, battery degradation, navigation, obstacle avoidance, communications, noise and emergency landing. But their delivery path is often cleaner because they travel between known points. Humanoids are exposed to every bit of human messiness.

This is why the fastest path to commercial humanoid delivery may be semi-structured buildings. A hotel can map floors, standardize elevator access, set robot-friendly paths and train staff. A hospital can designate routes. A mall can install robot lanes or pickup points. A residential compound can define handoff cabinets. The more the environment adapts, the sooner the robot works.

The fully general robot courier is a later step. It would need to operate across countless buildings without special preparation. That is not impossible, but it is far beyond a restaurant demo.

The most honest near-term forecast is layered adoption: service robots indoors, wheeled robots in controlled outdoor spaces, drones on fixed low-altitude corridors, and humanoids in selected public-facing roles where their shape is useful enough to justify the cost.

AI models are changing delivery, but logistics is still physical

Food delivery platforms already use AI long before a drone leaves a hub or a robot rolls through a mall. Order prediction, dispatch assignment, estimated arrival times, merchant ranking, fraud detection, rider routing and customer-service automation all shape the experience. The newer shift is that AI is moving from screens into machines.

Meituan-related research shows the platform depth behind consumer delivery. A 2025 arXiv paper on Meituan’s generative recommendation framework described MTGR as deployed on Meituan’s main traffic and handling recommendation at industrial scale. Another 2025 arXiv paper described a nationwide deployment of human activity recognition in the on-demand food delivery industry involving 500,000 couriers across 367 cities in China.

These systems do not look like robots, but they matter for robotics. A drone or robot delivery network needs demand prediction, dispatch, route allocation, failure handling and customer matching. AI models decide whether a drone should be assigned, whether a ground courier is better, whether a pickup point is overloaded, and whether weather or traffic changes the plan.

The mistake is to imagine physical AI as separate from platform AI. In reality, a drone is an endpoint in a larger decision system. The platform predicts demand. The merchant prepares goods. The dispatch system selects a mode. The robot executes a physical leg. The customer interface manages expectations. The safety system monitors risk.

That integration is where Chinese platforms have an edge. They already run high-frequency logistics at city scale. Adding machines is hard, but the software foundation exists. A startup with a drone but no order flow must create demand. A platform with demand can test machines against real operations.

Yet logistics remains stubbornly physical. A model can predict that a drone route will be faster. It cannot stop sudden wind. A dispatch system can choose a humanoid for a lobby route. It cannot guarantee that a child will not block the robot. A map can mark a path. It cannot remove spilled soup from a floor.

This is why automated delivery must be judged by service recovery. The question is not whether the machine works on a normal day. It is whether the system handles failure gracefully. Does it reroute the order? Refund the customer? Send a human courier? Land the drone safely? Notify the merchant? Protect the food? Log the incident for regulators?

Human couriers recover from failure constantly. They call customers, ask guards, move around obstacles and make judgment calls. Machines need explicit recovery paths. Without them, a single edge case can turn a fast delivery into a customer-service mess.

The physical world punishes brittle automation. China’s advantage is that it can expose systems to huge volumes of real tasks, but that also means failures become visible. The platforms that win will not be the ones with the most impressive demos. They will be the ones with the least dramatic failure rates.

Regulation is catching up with low-altitude traffic

Drone delivery cannot grow without airspace rules. China’s regulatory system is moving from permissive experimentation toward more formal oversight as the number of civil unmanned aircraft increases. CAAC reported in December 2025 that two mandatory national standards for civil unmanned aircraft would take effect on May 1, 2026, covering real-name registration and activation, and identification specifications for civil unmanned aircraft system operations.

The same CAAC notice said that in 2024 nearly 20,000 entities had obtained UAV operation certificates, registered UAVs exceeded 2 million, annual flight hours within the statistical scope surpassed 26 million, and as many as 26,000 UAVs were simultaneously in the air.

Those figures make regulation unavoidable. A handful of drone demos can be handled case by case. Millions of registered UAVs and thousands of operators require identification, monitoring and safety systems. Food delivery drones are only one part of that airspace, alongside inspection, agriculture, emergency response, mapping, entertainment and other commercial uses.

China’s low-altitude safety department, established by CAAC in 2026, adds another layer. It is responsible for development planning, safety coordination, dispatch platforms and flight-service station systems, according to the State Council portal.

For delivery platforms, regulation can be a burden and a moat. It raises compliance costs. It also favors companies large enough to build safety systems, apply for licenses, integrate with dispatch platforms and document operations. A small drone startup may struggle with regulatory overhead. A giant platform can spread compliance costs across many routes.

China Daily reported in April 2025 that Meituan’s fourth-generation drone passed a CAAC regulatory review, earning what it described as the country’s first operating certificate for nationwide low-altitude logistics coverage. The report said the license would allow Meituan to launch regular commercial drone delivery services across China.

That certificate matters because local pilots are not enough. A company operating across major cities needs a framework that travels. Nationwide coverage does not mean drones will appear everywhere immediately. It means the regulatory foundation is broader than one district.

Regulation will also shape design. If drones must transmit identification information, manufacturers need hardware and software compliance. If routes require dispatch integration, platforms must connect systems. If medium and large drones face stricter airworthiness rules, companies may favor lighter vehicles for urban food delivery. If nighttime operations require extra approvals, the economics of evening demand change.

Public trust depends on this unseen layer. Customers may enjoy fast delivery, but residents will object if drones are noisy, unsafe or poorly managed. Cities will support low-altitude logistics only if they can show that safety and accountability exist. The growth of drone food delivery is therefore a governance story as much as a technology story.

Safety, noise and public trust will decide scale

A delivery drone is small, but it operates in shared space. That makes safety and public trust decisive. A drone crash, battery fire, dropped package or noise complaint can damage public acceptance faster than a thousand successful deliveries can build it.

Urban drone delivery has several risk categories. The aircraft may fail mechanically. Communications may drop. Weather may change. A package may detach. A landing zone may be blocked. People may enter restricted areas. Birds, wires and buildings can complicate flight. The system must handle each risk without improvising like a human.

This is why fixed routes and kiosks matter. They reduce uncertainty. A drone flying to a known station can be monitored more easily than one trying to deliver to random balconies. A winch-drop system can avoid landing near people. A smart hub can control loading and pickup. A route approved by regulators can be inspected and adjusted.

Noise may be just as important as crash risk. People tolerate delivery scooters because they are familiar, even when they are loud. Drones introduce a different sound, often overhead, which can feel more intrusive. A service that works technically may still fail socially if residents dislike the noise.

Weather also affects trust. Customers do not only ask whether the drone can fly in rain. They ask whether the order will arrive as promised. Meituan’s drone business has reportedly expanded services at night and in the rain, according to Yicai’s report citing Mao Yinian.

That is operationally important. Food delivery peaks do not wait for perfect weather. Rain often increases delivery demand. If drones only fly in ideal conditions, their value is limited. If they fly safely in moderate rain or at night, they become more useful. But each expansion of operating conditions increases the safety burden.

Humanoid and ground robots face public trust in another form. A robot rolling through a community must not block elderly pedestrians, frighten children, trap pets, record sensitive images without safeguards or fail in a way that requires constant rescue. A humanoid robot has additional social weight because it looks like a person or invites person-like interaction.

Restaurants and robot-themed venues are low-risk settings for public familiarity. Streets, hospitals and residential compounds are higher trust environments. A machine moving through a hospital corridor must meet a different standard than a robot dinosaur entertaining diners.

Data privacy will become more serious as robots gain cameras, microphones and maps. A delivery drone may capture imagery. A ground robot may scan building entrances. A humanoid may process speech. Platforms will need clear rules for data retention, access, security and customer consent.

Public trust will not come from saying the machines are advanced. It will come from boring reliability: safe routes, low noise, clear pickup instructions, fast refunds, visible accountability and few surprises.

The delivery chain is becoming more modular

The traditional food-delivery chain is simple: restaurant, courier, customer. China’s automated delivery chain is becoming modular. Different machines and humans handle different legs, and the platform coordinates the handoff.

A drone route might involve a merchant, local runner, drone hub, aircraft, destination kiosk, customer and support team. A wheeled robot route might involve a depot, autonomous vehicle, community transfer station and final courier. A restaurant robot might involve kitchen staff, a tray robot, a table handoff and a human server who handles exceptions.

This modularity changes the economics. A human courier is flexible but expensive in time. A drone is fast on a specific path but inflexible. A robot is consistent in a mapped area but poor at exceptions. A platform can mix them to reduce the weakest parts of each.

A modular chain also creates more surfaces for failure. Every handoff can go wrong. The food may be loaded late. The drone may miss a slot. The kiosk may be full. The customer may not collect. The courier may not arrive for the final leg. A bag may be assigned to the wrong compartment. Automation does not remove coordination problems; it creates new ones.

This is where platform software becomes central. The system must know item status at every point. It must assign orders to the correct mode, update customers, protect food quality and recover from delays. A drone flying perfectly is useless if the order sits too long at the origin hub.

Modularity also affects packaging. Food designed for scooter delivery may not be ideal for drone delivery. Liquids must be sealed. Hot food needs insulation. Fragile items need shock protection. Weight limits shape menu availability. Merchants may need platform-approved packaging for drone routes.

This could influence restaurant operations. A merchant near a drone hub may create drone-friendly menu bundles: drinks, snacks, sealed meals, medicine, convenience goods. The platform may rank items based on delivery suitability. Customers may see only drone-eligible products for certain destinations.

Meituan’s Keeta Drone page says its service offers access to more than 160,000 product choices across regions as of March 2026, showing that aerial delivery is already framed as instant retail, not only meals.

That matters. Food delivery may be the entry point, but the business case improves when the same network carries more categories. A drone route that only handles lunch is underused. A route that handles coffee, pharmacy items, documents, lab samples, emergency supplies and snacks has more chances to earn its infrastructure.

The future delivery network looks less like a courier replacement and more like a dispatch fabric, with humans, drones, ground robots, lockers, hubs and restaurants connected through software.

Merchants get visibility, but not automatic profit

Restaurants and shops are central to the automated delivery story, but their incentives are not identical to platform incentives. A platform wants route density and consumer engagement. A merchant wants profitable orders that do not disrupt kitchen flow.

Drone delivery can expand a merchant’s catchment area. A café near Wujiaochang can reach customers in Huangxing Park more quickly. A restaurant near a scenic area can serve tourists without opening a stall. A pharmacy can send urgent items to a hospital point. These are real benefits.

But merchants also face costs. They may need special packaging. They may need staff to prepare orders within tighter flight windows. They may face customer complaints if the drone handoff creates confusion. They may need to adjust menus to avoid items that travel poorly by air.

A platform may subsidize early adoption, but long-term economics matter. If drone delivery brings incremental demand at normal margins, merchants will like it. If it mostly shifts existing orders into a more complex channel, enthusiasm may fade.

The same applies to robot restaurants. A robot-themed venue can attract crowds because novelty is part of the product. A normal restaurant may not benefit from buying or leasing robots unless they reduce labor strain or improve service. A tray robot that frees staff from walking may help. A humanoid that draws photos but slows service may not.

China Daily reported that Beijing’s robot-themed restaurant took bookings through Dianping and Meituan, with many people waiting to try the experience. That is a strong novelty case. It does not automatically translate to every restaurant.

Merchants will judge automation by four questions. Does it bring new customers? Does it lower service burden? Does it protect food quality? Does it avoid platform fees or operational demands that eat the margin? A yes to the first two may be enough for some. A no to the last two can kill adoption.

Automation may also change merchant visibility. A shop connected to a drone route may appear more prominently for customers at destination points. A restaurant with robot-friendly service may gain social media attention. A merchant outside the route may become less visible in a park or campus destination. Delivery infrastructure can reshape competition among nearby businesses.

This is already true in platform delivery. Ranking and distance affect order volume. Drone hubs and pickup stations add another layer. The merchant closest to the hub may win. The merchant with the right packaging may be eligible. The merchant with high preparation reliability may be favored by dispatch algorithms.

Automated delivery is not neutral infrastructure. It can shift local commerce toward merchants that fit the machine network.

That raises fairness questions. Will small restaurants be able to join drone delivery routes? Will packaging requirements favor chains? Will platform rankings clearly explain why certain products are available by drone and others are not? These questions will grow as automated routes become normal.

Riders are not disappearing, their jobs are being rearranged

The image of drones and robots replacing riders is too simple. Riders remain central to China’s delivery system because they handle the messy edge of service. What changes is the mix of tasks.